The tale of neobanks, the plucky upstarts in the financial sector, has been a wild ride. Over recent years, economic headwinds and soaring interest rates have created turbulent skies for these digital disruptors. The era of “growth at all costs” is fading, with only a small fraction of neobanks showing profits. In this new landscape, the focus has sharply shifted towards achieving sustainable profitability.

At Elsewhen, we observe this trend deepening further, with neobanks shifting towards “full-service” digital banking models. To acquire a larger share of customer wallets, neobanks should now enrich their proposition, income sources, and product suite – with credit cards, personal loans, and insurance being just the beginning.

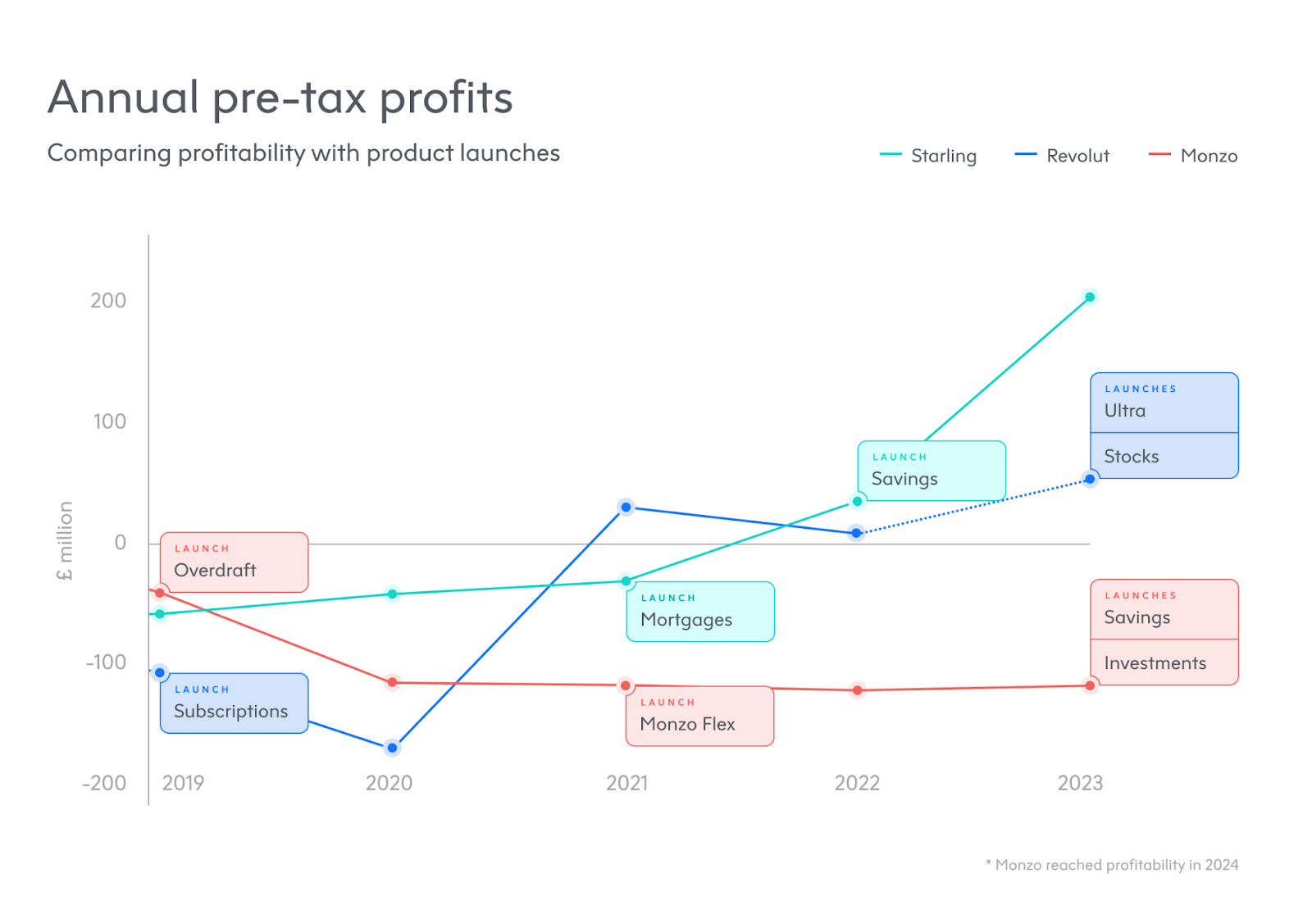

The Winds of Change

Neobanks are evolving. They’re moving from single-product simplicity to embracing diverse revenue streams. Notable players like Starling Bank, Monzo, and Revolut are capitalising on lending products and subscription models to bolster their financial standings. For instance, Revolut has expanded its offerings with a $45-a-month Ultra account and a promising retail media arm aiming for an extra £300 million in revenue. Monzo, on the other hand, ventured into investments and redefined its subscription tiers.

The Multi-Product Challenge

Initially, neobanks thrived on simplicity—one market, a couple of customer segments, and a handful of basic products. This straightforward approach was mirrored in their sleek, user-friendly apps. But as they scale up and add products like credit cards and loans, maintaining that seamless user experience becomes a Herculean task.

For digital teams, the challenge lies in balancing the need to promote new products while preserving the user-centric experience that set them apart from traditional banks. Let’s delve into how Nubank, a Brazilian giant, navigated this transformation.

Nubank’s Journey: From Humble Beginnings to a Powerhouse

Nubank burst onto the scene in 2014 with a fee-free credit card, swiftly capturing the hearts of unbanked and underbanked Brazilians. Fast forward to today, Nubank boasts over 100 million customers and a market valuation of $51 billion.

As Nubank expanded, it added current accounts, insurance, investments, and more. The secret to their success? A model that merges customer-centricity with robust financial performance. By focusing on active customers—those who generate revenue within 30 days—and average revenue per active customer (ARPAC), Nubank has grown both its user base and profitability. In 2023, 83% of Nubank’s customers were active, and ARPAC surged to $11.4, driving net profits of £1 billion.

Simplifying Complexity: Nubank’s Approach

Nubank’s digital team faced the monumental task of scaling their product offerings while maintaining a clean, user-friendly interface. Their solution? A redesigned app with three intuitive tabs: day-to-day transactions, financial planning, and discovery. This structure not only streamlined navigation but also provided a dedicated space for new products.

To keep product discovery relevant, Nubank implemented tailored suggestions based on user behaviour. This approach ensured that customers received helpful recommendations without cluttering the interface with promotional content.

Lessons from Nubank

Nubank’s journey underscores the importance of balancing customer experience with business objectives. Here are a few strategies that other neobanks can adopt:

- New Customer Journeys: Create onboarding processes that handle additional products, like credit checks for loans.

- Redesigning UI/IA:: Develop interfaces that can accommodate multiple products without overwhelming users.

- Enhanced Discovery: Implement personalised recommendations to help users find relevant products.

- Decision-Making Frameworks: Establish metrics that balance customer needs with business goals.